Hospitals, Medicaid Insurers Still Face an Ugly Future: Gadfly

(Bloomberg Gadfly) —Trumpcare’s chances of becoming law took a big hit this week. But the hospitals and Medicaid insurers directly in its path can’t rest easy.

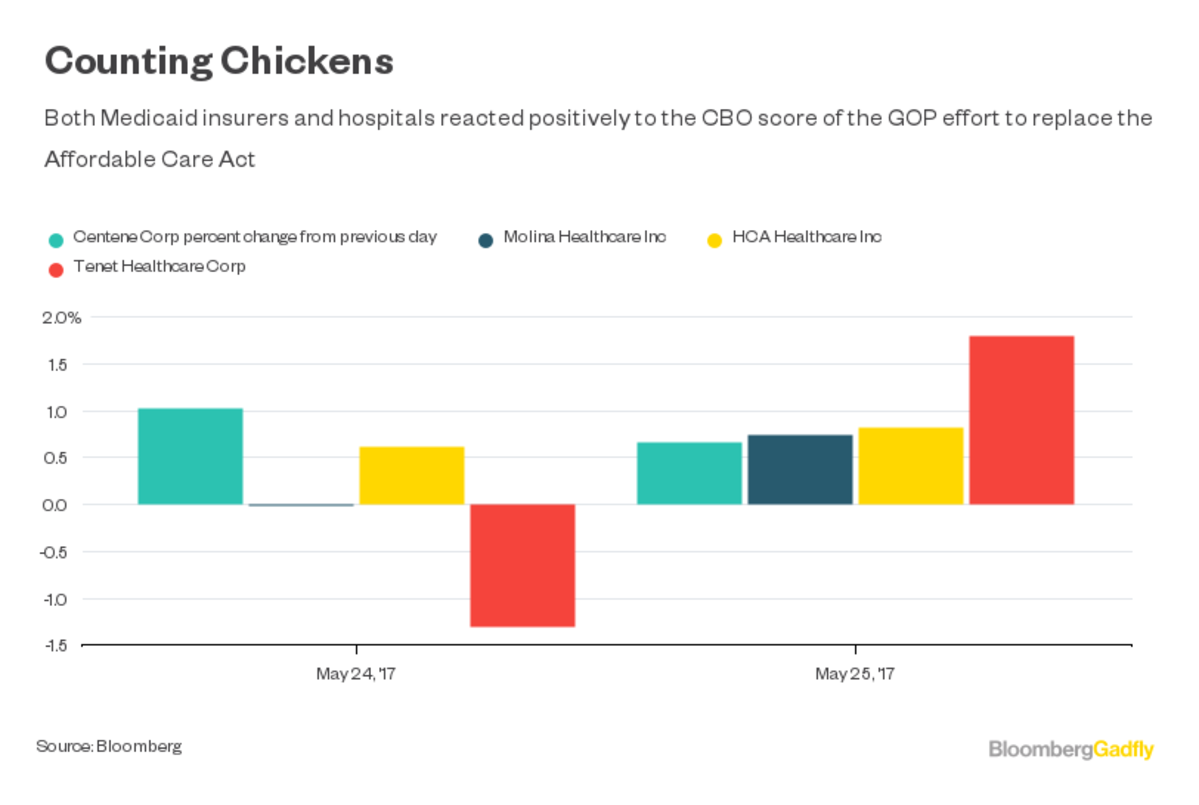

Shares of such companies rose on Thursday, presumably cheering the Congressional Budget Office’s score of the House-passed version of the American Health Care Act. The CBO score, released Wednesday evening, raised substantial new roadblocks to Trumpcare’s passage in the Senate. It said the law would take health care from 23 million Americans, barely improving on the 24 million in the CBO’s score of an earlier version of the AHCA. It also warned the law would destabilize the individual insurance market and gut pre-existing condition protections for one-sixth of Americans.

But this latest score still leaves a huge amount of uncertainty and a disquieting set of possible outcomes for hospitals and insurers.

The possibility of something close to the AHCA becoming law — unlikely, but still possible, given the intense pressure to get this legislation done so the GOP can move on to tax reform — looks more negative than ever for these companies.

The biggest reason the new CBO score is worse than its score of an earlier version of the bill, and why the bill has gotten scarier to hospitals in particular, is an addition called the MacArthur amendment. This lets states apply for waivers to let insurers raise premiums for people with pre-existing conditions and to not force insurers to cover so-called essential health benefits (EHBs).

The CBO expects states where one-sixth of Americans live will take substantial waivers. As a result, premiums will go down for young and healthy people, albeit for far skimpier coverage and with higher out-of-pocket costs.

Amount the AHCA Cuts From Medicaid: $800 Billion

Premiums are expected to skyrocket for older and low-income Americans in all states. They will increase even more for people with pre-existing conditions in states that get substantial insurance-rule waivers, to the point where the CBO expects many won’t be able to afford insurance. Another one-third of Americans will live in states that only modify some regulations; they’ll have similar issues, just to a lesser extent.

That’s not great for hospitals. Not only would they be on the hook for any care they provide to 23 million new uninsured people, they also face the effects of many more Americans having insurance that discourages them from getting care.

This comes on top of a bill that was already rough on the sector. The worst part of it was basically unchanged in the new CBO score: a massive $800 billion in Medicaid cuts over the next 10 years. Those cuts account for 14 million of those 23 million that would be newly uninsured. That $800 billion in missing coverage will have to be made up somewhere, and much if will come from the pockets of hospitals and other health-care provider and Medicaid-focused insurers.

The size of those Medicaid cuts, the desire to protect people with pre-existing conditions, and a big projected jump in the number of uninsured Americans mean AHCA passage is probably the least likely outcome of all this.

But even if the Senate does substantially change the bill, there’s a lot of uncertainty about how much it will actually improve its effects.

In order to use the budget reconciliation process and avoid a filibuster in the Senate, a repeal-and-replace bill must knock at least $2 billion from the deficit. The AHCA so far clears that bar easily, cutting a cumulative $119 billion from the deficit over a decade.

But with every set of amendments, the bill has saved less money. Medicaid is by far the biggest cost-saver; scaling back its cuts would be expensive, leaving the Senate with less wiggle room. Other changes the Senate is considering to soften the bill’s impact — from automatically enrolling people in catastrophic insurance coverage, to boosting funds to lower premiums for those with pre-existing conditions, to more-generous tax credits — will be pricey, too, if they’re to have any real effect.

Trimming the Medicaid cuts by $100 billion or so, to squeak in under reconciliation rules, would do relatively little to help hospitals and insurers. Scaling back the tax cuts in the bill would allow for more spending on Medicaid, but would be politically difficult.

All of this suggests that whatever comes out of the Senate as it writes its bill over the next few weeks will not reverse as many of the scary things in the AHCA as hospitals and insurers hope.

It’s also very possible, given its two-vote margin of error, the Senate won’t pass a bill at all. Majority leader Mitch McConnell recently conceded as much. That would mean the ACA will remain the law of the land. That’s arguably the best scenario for many in health care. But even that result has the potential to be ugly. The Trump administration has repeatedly delayed a decision on funding cost-sharing subsidies that help low-income people afford insurance on the ACA’s individual exchanges. Those delays and the resulting uncertainty have created potential instability in a number of state markets.

And there’s little to suggest the GOP would do much to support the ACA and the health-care providers that depend on it, or Medicaid insurers such as Centene Corp. and Molina Healthcare Inc., which have a large presence in the ACA’s insurance exchanges.

Regardless of how this drama plays out, there’s a very good chance health-care providers and Medicaid insurers will lose out.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

{kind=link}

No Comment