Israelis Are Getting a Taste for the Good Life — and Leverage

(Bloomberg) —If you’ve been driving on Israel’s roads over the past decade, you’ve probably noticed that every year the highways get more congested and the cars flashier.

Households that used to have just one car now allow themselves more. Changes are evident inside Israeli homes too, with a proliferation of tablets, smart-phones and flatscreen TVs. The consumption craze isn’t just for the upper-middle class: It’s poorer Israelis that are delivering the sharpest surge, according to a recent Finance Ministry study.

While interest rates remain anchored at record lows, workers are taking advantage of pay increases and lower borrowing costs to upgrade everything from computers to cars. That’s propelling economic growth, but also leverage in a country that until recently had been rather conservative about borrowing money.

So far, the consumption boom has been good news. The economy grew 4 percent last year, far above the developed-nation average. But the leverage is starting to worry policy makers.

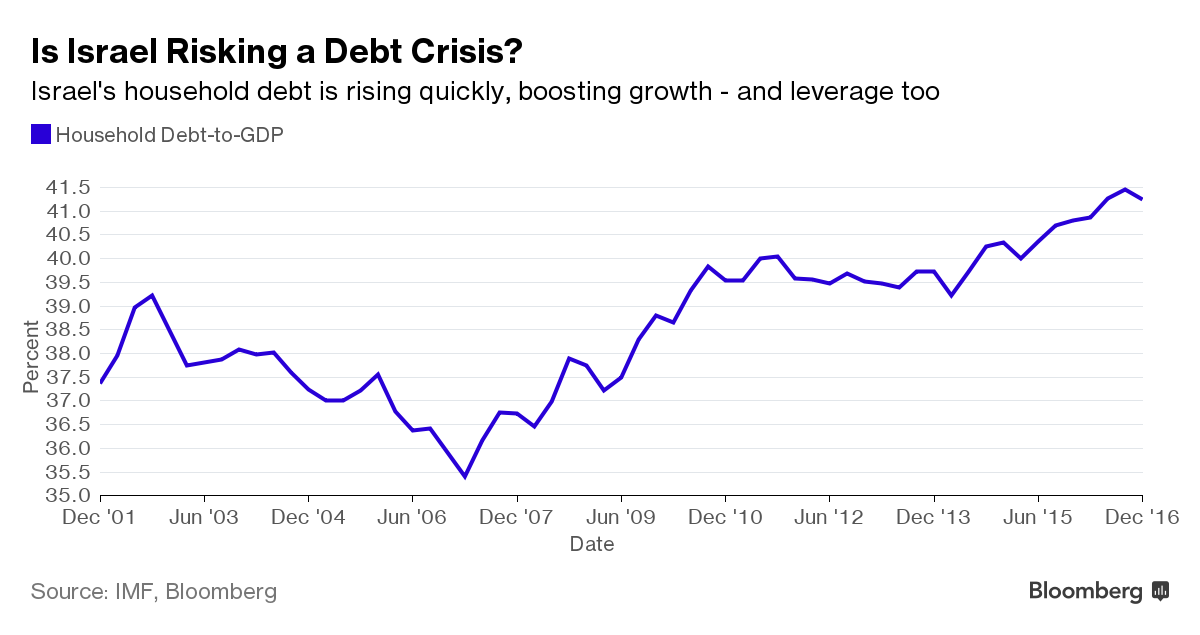

Yoel Naveh, the Finance Ministry’s chief economist, warned earlier this month that the 9 percent growth in household credit last year made him think of the U.S. sub-prime crisis. His comments came after Bank Supervisor Hedva Ber warned that the financial system may be adding too much risk from consumers.

“Credit is like salt in food: Food with no salt is tasteless, but too much salt tastes bad and is unhealthy,” she said at a late-May press conference in Tel Aviv. “If we think that the problem is persisting and growing, we’ll intervene as necessary.”

Audits of Israeli banks last year revealed a sharp increase in consumer defaults, Ber said. Though the banks remain strong — they weathered the 2008 financial crisis without any bankruptcies — risks have increased, Ber said.

Politicians are warming to the issue: In a recent parliamentary hearing, lawmaker Zehava Galon of the left-wing Meretz Party said she was concerned by a sharp increase in personal bankruptcy filings after household loans rose 23 percent in the last three years.

For now, the Bank of Israel, which is fueling the credit growth with its 0.1 percent benchmark rate, isn’t too concerned. A central bank official told the parliamentary hearing that Israeli debt levels are still low compared to other nations. Even so, he warned that government reforms to bolster competition in the credit industry could exacerbate the situation.

There also has been a rise in non-banking loans, which are harder for the government and central bank to track. Ber noted that her 13-year-old son recently received a text message offering him a loan, a common way to attract borrowers in Israel.

Few Israelis are complaining, however, as they enjoy more vacations, better cars and fancier gadgets. And the consumption craze isn’t moving the dial on inflation, which remains below the government’s 1 percent to 3 percent target as competition-boosting reforms drive down prices and a strengthening currency cools inflationary pressures.

One worry is that consumption-driven growth may give the government a false picture of the economy’s strength and its ability to generate tax receipts. Most economists agree that Israel, a country of just 8.5 million people, needs to develop its export industry to grow in a sustainable way, an expansion that’s being challenged by a currency that can’t seem to stop strengthening.

“Expanding demand is healthy and natural as unemployment is low, house prices are high, so there’s a wealth effect leading to growing consumption,” said Michael Sarel, former chief economist at the Finance Ministry. “But it’s unsustainable to rely on this kind of consumption for growth.”

{kind=link}

No Comment